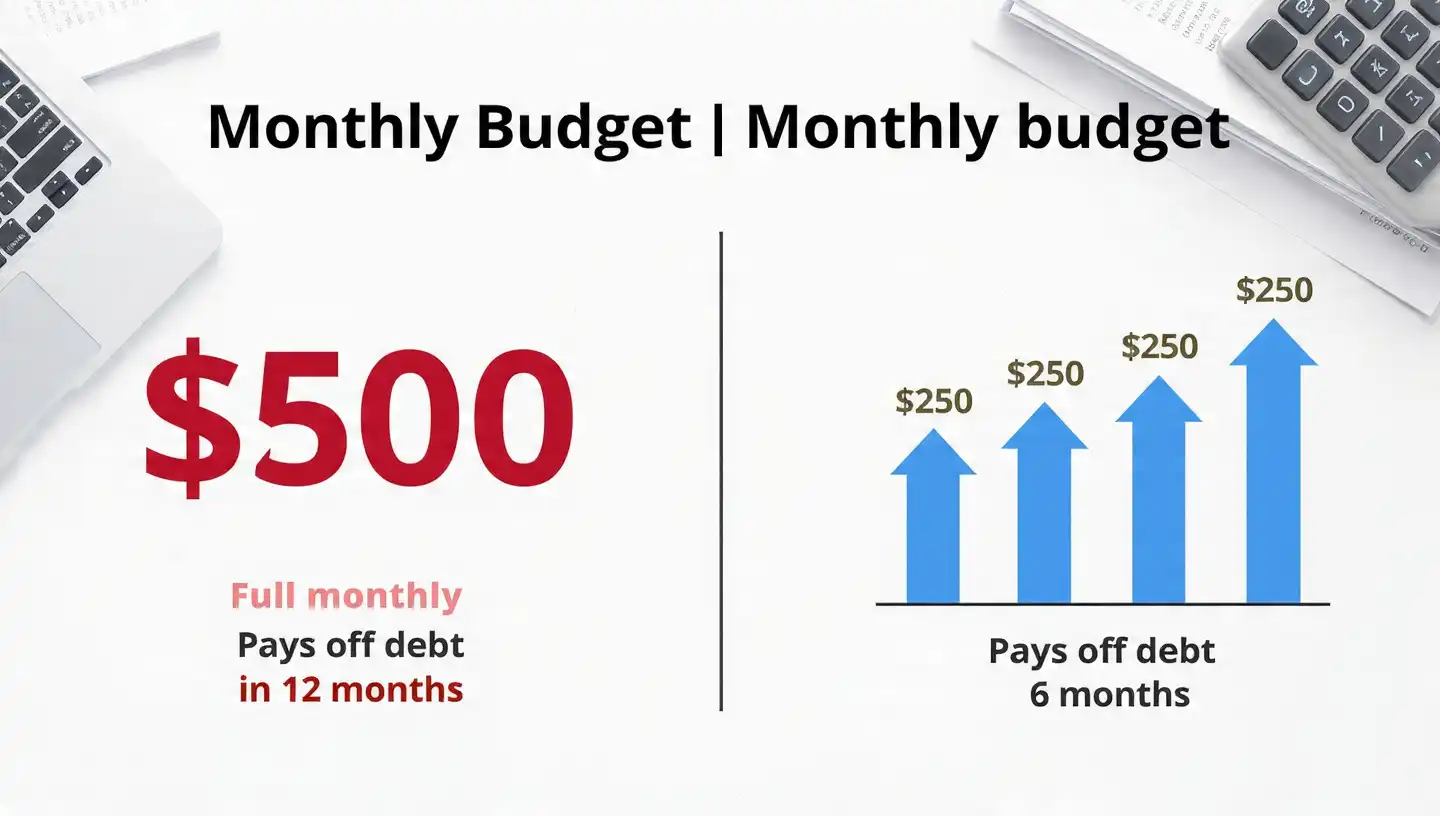

Break-Even Refinance Calculator

Calculate exactly when your refinance costs are recovered.

Bi-Weekly Savings Calculator

Visualize interest saved by switching to bi-weekly payments.

Recast vs Refinance Calculator

Compare lump-sum payment strategies vs getting a new loan.

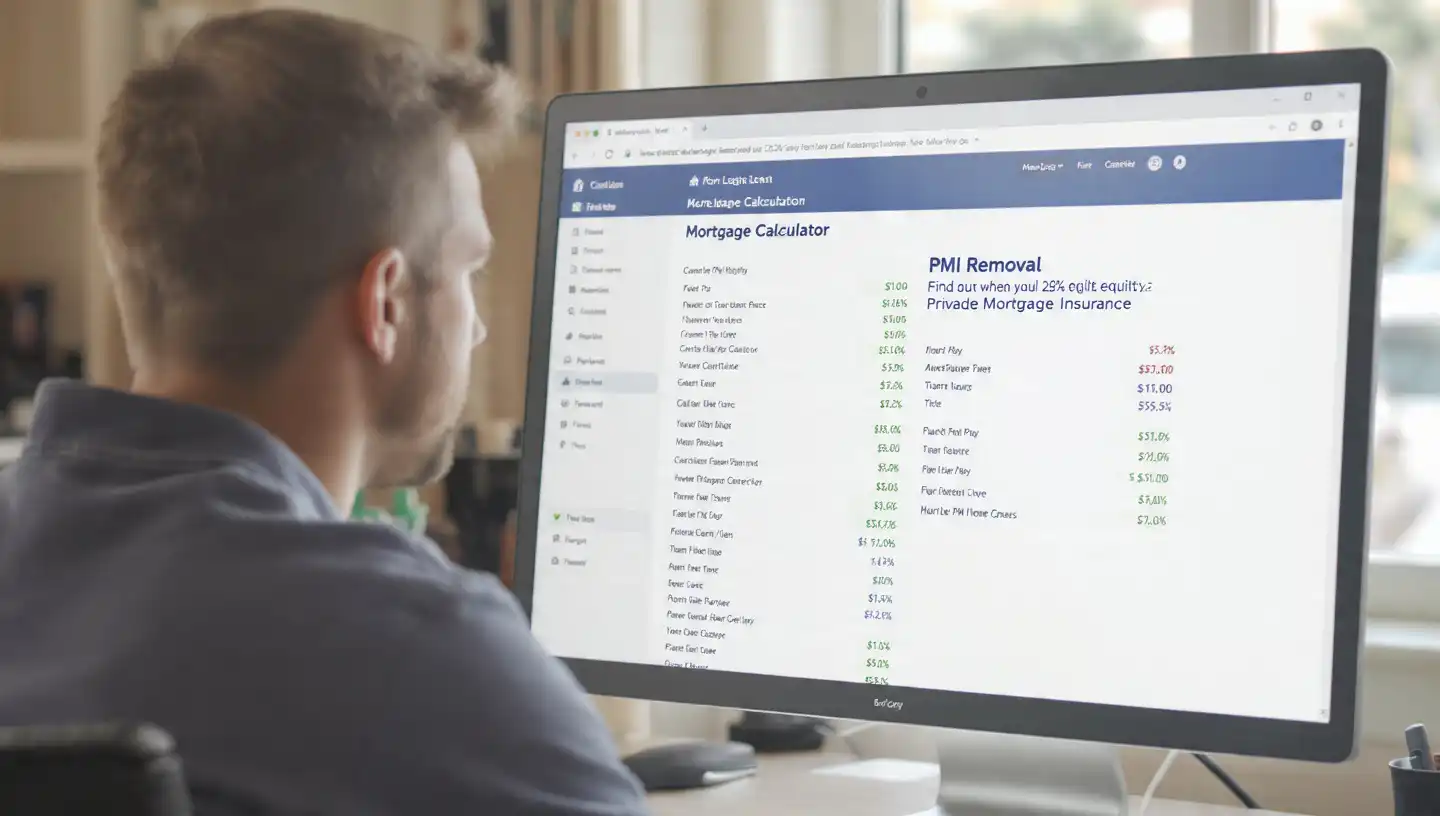

PMI Removal Calculator

Project when you will reach 20% equity to remove mortgage insurance.

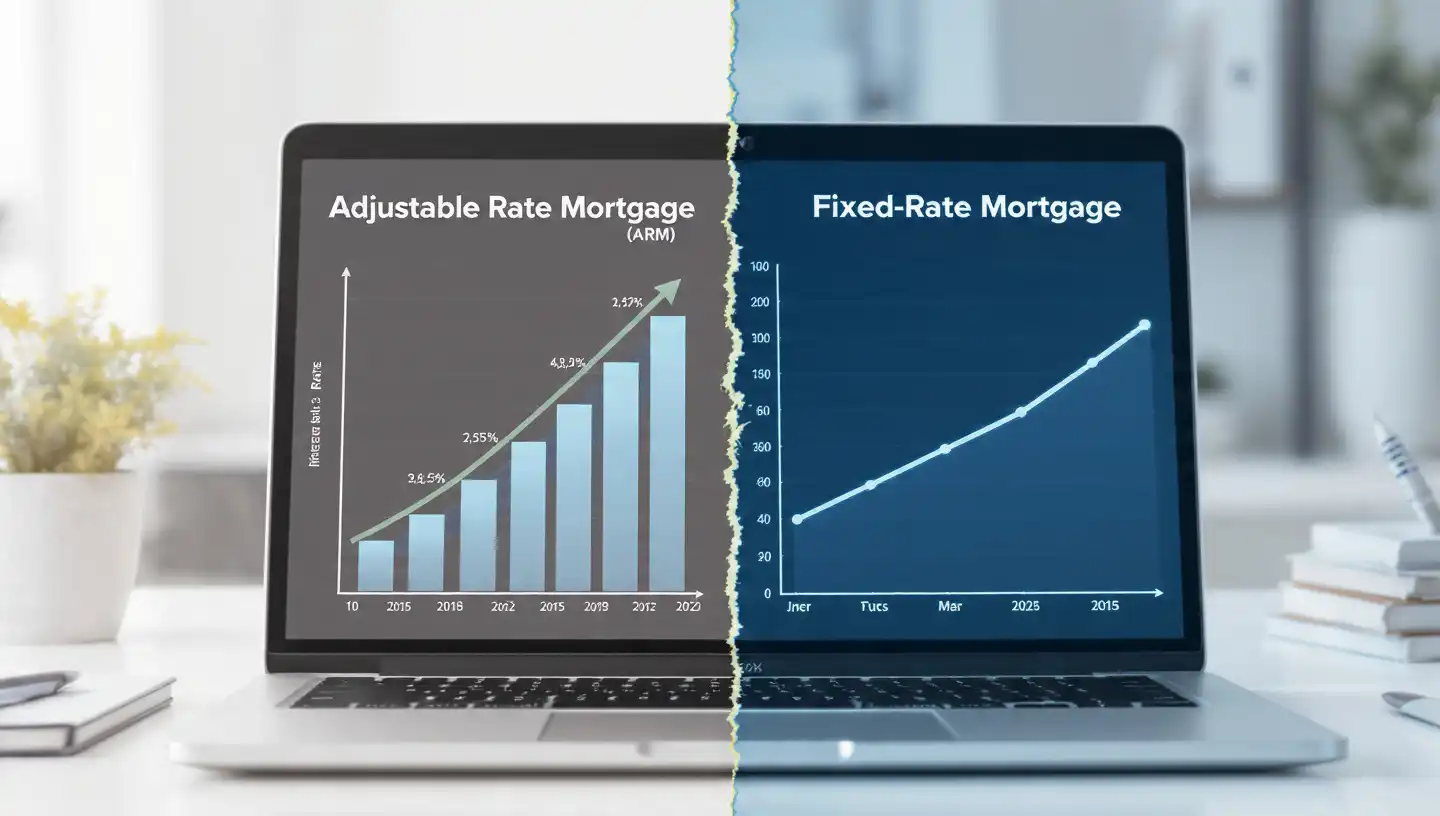

ARM vs Fixed Rate Calculator

Analyze worst-case scenarios for Adjustable Rate Mortgages.

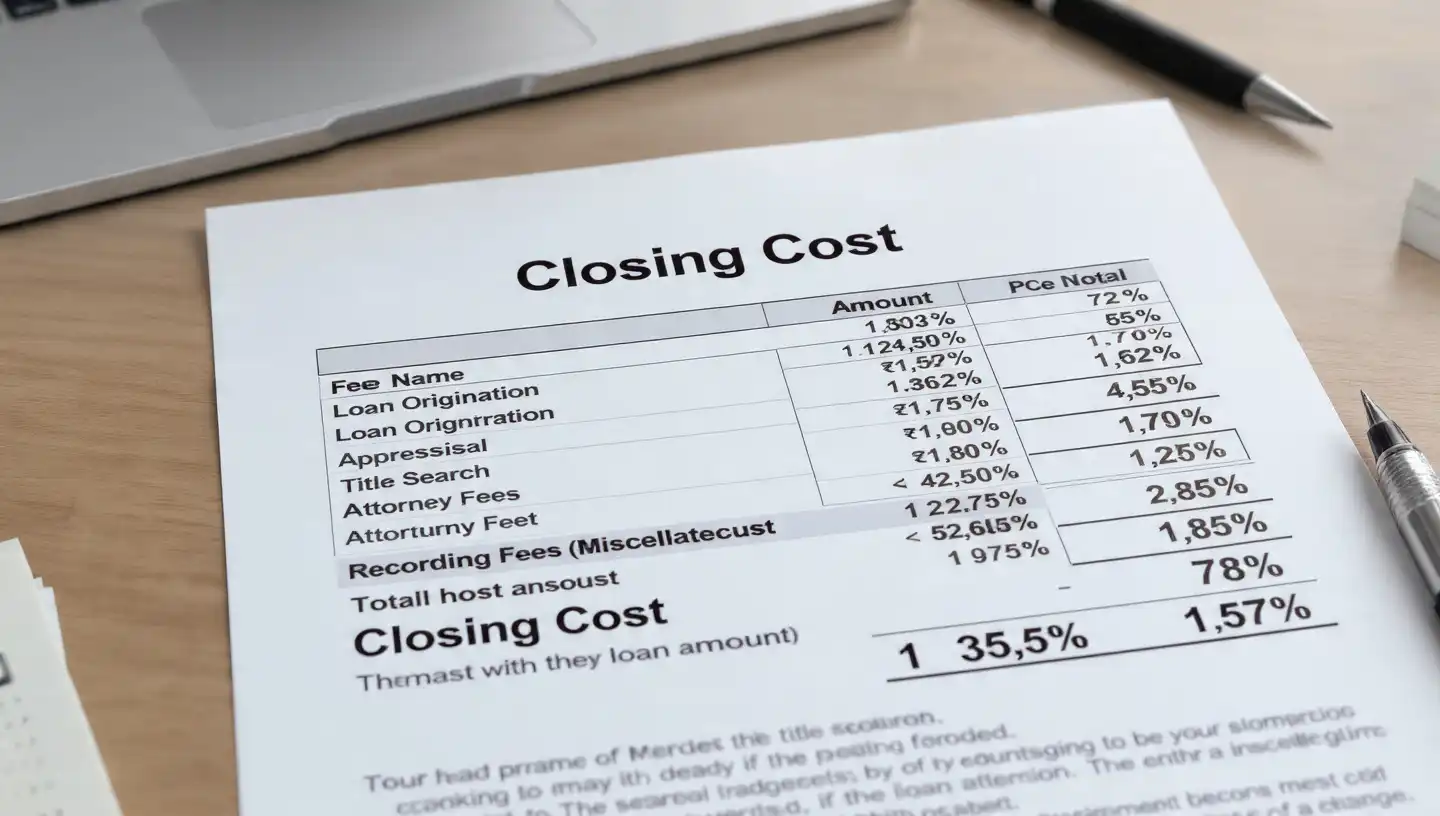

Closing Cost Estimator Calculator

Estimate title fees, taxes, and recording fees by state.

Mortgage Refinancing Guide

Refinancing involves replacing your current mortgage with a new one to achieve better terms. Whether your goal is to lower your monthly payment, pay off your home faster, or tap into your home's equity, understanding the numbers is critical.

Key Strategies

- Rate & Term Refinance: Change your interest rate or loan term (e.g., 30-year to 15-year) to save interest.

- Cash-Out Refinance: Borrow more than you owe and take the difference in cash for high-interest debt consolidation or home improvements.

- Break-Even Analysis: Always calculate how many months of savings it will take to recoup your closing costs.

Frequently Asked Questions

How much does it cost to refinance?

Closing costs typically range from 2% to 6% of your loan amount. This includes appraisal fees, title insurance, and origination fees. It's crucial to calculate your 'break-even point' to ensure the monthly savings justify these upfront costs.

Does refinancing hurt my credit score?

Temporarily, yes. When you apply, lenders perform a hard inquiry, which may drop your score by a few points. However, consistent payments on the new loan and a better debt-to-income ratio can improve your score over time.

What is the difference between refinancing and recasting?

Refinancing replaces your existing loan with a new one (new rate, new term). Recasting keeps your existing loan/rate but re-amortizes the balance after you make a large lump-sum payment, strictly to lower monthly payments.